Whether to open a claim

Opening a claim has consequences. It will appear on your insurance record for five years, your insurance policy might not get renewed, and it can be hard to maintain sufficient coverage at a reasonable rate. If the damage is limited, you might prefer to pay out of pocket.

Before you open a claim, you should consult with your insurance agent to make sure that the damage is covered under your policy. Sudden and accidental damage is typically covered, such as a roof that gets damaged during rain, a burst pipe, or an overflowing bathtub, while long-term leaks are typically excluded.

The adjuster

After you open a claim, the insurance company will send someone over to estimate the damage. That person is called the adjuster. They will take photos, sketch the floor plan,create an itemized list of required repairs for every room, and create a list of damaged items. The adjuster will only consider visible damage, and it is not unusual that the actual damage is 2-5 times higher than the initial estimate. The adjuster will update the estimate as additional information becomes available.

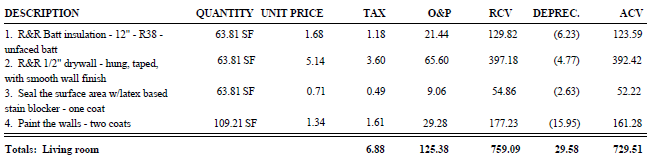

Xactimate

Most adjusters use a software tool called Xactimate to estimate the cost of repairs. This software provides an up-to-date database of regional pricing. For example, it knows the cost per square feet of drywall, the cost to prep for paint, and the cost to detach and reset a toilet. When you first get the Xactimate estimate from your adjuster, you may think you have a good understanding of the scope of work and how much it should cost.

- Closets require more labor per square foot than large rooms.

- Blending new into existing drywall takes considerable time and effort not reflected in Xactimate.

- Plumbing, electric work, clean-up, and project supervision are poorly estimated by Xactimate.

- Door and window casing is meant to cover the gap between the drywall and the door and window. When drywall is removed, the new drywall should go under the casing. You almost always have to remove the casing for this. It is considerably easier to take a shortcut and install drywall against the casing and caulk the gap, but this is probably not what you want.

Replacement value or actual cash value

Most insurance policies cover replacement value. If a floor is a hundred years old, full of dents and gaps, and water damaged to the degree that it cannot be repaired, most insurance policies will pay for a brand new floor. However, that does not mean that they will immediately pay the costs of the new floor. Initially, they will only pay out the current value (actual cash value or ACV). Only if you go ahead and replace the floor, they will pay out the additional amount (replacement cost value or RCV). The difference between RCV and ACV is called the depreciation. You can only recover the depreciation by actually spending the money on an identical or similar item or repair. The process to recover the depreciation differs for repairs and personal property.

Recovering depreciation for personal property

For personal property you can typically recover depreciation on individual items. You will receive the replacement value of items you replace, and actual cash value for items that you dispose of.

Recovering depreciation for repairs

You can typically only recover the depreciation on all repairs together. That means if you only go ahead with a few repairs, that you lose money. A small example can clarify this. Suppose two rooms are damaged, the actual cash value of the damaged items is $1000 per room, and the replacement value of the damage is $1500 per room. Initially, the insurance company will pay $2000 (ACV). If you spend $1500 to repair one room, the insurance company will not pay any additional amount, since the total you spend on repairs is less than what has already been paid out.

If you plan to make an RCV claim for repairs:

- Pay your contractors by check. Insurance companies do not recognize cash payments.

- Repair all damage. You leave money on the table if you make only a few repairs.

- If you choose to do any work yourself, know that insurance companies do not compensate you for your time.

The mortgage holder

If you have a mortgage, any insurance payments for repairs typically go to the mortgage holder. They have an interest that your home gets restored to the original value. They will periodically check progress, and release money to you as the repairs progress.